Value of $70,000 from 2005 to 2025

$70,000 in 2005 is equivalent in purchasing power to about $114,623.30 today, an increase of $44,623.30 over 20 years. The dollar had an average inflation rate of 2.50% per year between 2005 and today, producing a cumulative price increase of 63.75%.

This means that today's prices are 1.64 times as high as average prices since 2005, according to the Bureau of Labor Statistics consumer price index. A dollar today only buys 61.070% of what it could buy back then.

The inflation rate in 2005 was 3.39%. The current inflation rate compared to the end of last year is now 2.39%. If this number holds, $70,000 today will be equivalent in buying power to $71,673.51 next year. The current inflation rate page gives more detail on the latest inflation rates.

Contents

⌃

| Cumulative price change | 63.75% |

| Average inflation rate | 2.50% |

| Converted amount $70,000 base | $114,623.30 |

| Price difference $70,000 base | $44,623.30 |

| CPI in 2005 | 195.300 |

| CPI in 2025 | 319.799 |

| Inflation in 2005 | 3.39% |

| Inflation in 2025 | 2.39% |

| $70,000 in 2005 | $114,623.30 in 2025 |

Buying power of $70,000 in 2005

This chart shows a calculation of buying power equivalence for $70,000 in 2005 (price index tracking began in 1635).

For example, if you started with $70,000, you would need to end with $114,623.30 in order to "adjust" for inflation (sometimes refered to as "beating inflation").

When $70,000 is equivalent to $114,623.30 over time, that means that the "real value" of a single U.S. dollar decreases over time. In other words, a dollar will pay for fewer items at the store.

This effect explains how inflation erodes the value of a dollar over time. By calculating the value in 2005 dollars, the chart below shows how $70,000 is worth less over 20 years.

According to the Bureau of Labor Statistics, each of these USD amounts below is equal in terms of what it could buy at the time:

This conversion table shows various other 2005 amounts in today's dollars, based on the 63.75% change in prices:

| Initial value | Equivalent value |

|---|---|

| $1 dollar in 2005 | $1.64 dollars today |

| $5 dollars in 2005 | $8.19 dollars today |

| $10 dollars in 2005 | $16.37 dollars today |

| $50 dollars in 2005 | $81.87 dollars today |

| $100 dollars in 2005 | $163.75 dollars today |

| $500 dollars in 2005 | $818.74 dollars today |

| $1,000 dollars in 2005 | $1,637.48 dollars today |

| $5,000 dollars in 2005 | $8,187.38 dollars today |

| $10,000 dollars in 2005 | $16,374.76 dollars today |

| $50,000 dollars in 2005 | $81,873.78 dollars today |

| $100,000 dollars in 2005 | $163,747.57 dollars today |

| $500,000 dollars in 2005 | $818,737.84 dollars today |

| $1,000,000 dollars in 2005 | $1,637,475.68 dollars today |

Inflation by City

Inflation can vary widely by city, even within the United States. Here's how some cities fared in 2005 to 2025 (figures shown are purchasing power equivalents of $70,000):

- San Diego, California: 3.73% average rate, $70,000 → $140,309.43, cumulative change of 100.44%

- Tampa, Florida: 3.07% average rate, $70,000 → $124,344.51, cumulative change of 77.64%

- Miami-Fort Lauderdale, Florida: 3.03% average rate, $70,000 → $127,235.50, cumulative change of 81.76%

- Seattle, Washington: 2.93% average rate, $70,000 → $124,688.09, cumulative change of 78.13%

- Denver, Colorado: 2.88% average rate, $70,000 → $120,115.45, cumulative change of 71.59%

- Phoenix, Arizona: 2.81% average rate, $70,000 → $118,593.44, cumulative change of 69.42%

- San Francisco, California: 2.79% average rate, $70,000 → $121,383.20, cumulative change of 73.40%

- Atlanta, Georgia: 2.60% average rate, $70,000 → $116,928.22, cumulative change of 67.04%

- Dallas-Fort Worth, Texas: 2.53% average rate, $70,000 → $115,420.49, cumulative change of 64.89%

- New York: 2.40% average rate, $70,000 → $112,546.84, cumulative change of 60.78%

- Boston, Massachusetts: 2.35% average rate, $70,000 → $111,367.41, cumulative change of 59.10%

- Minneapolis-St Paul, Minnesota: 2.34% average rate, $70,000 → $108,698.29, cumulative change of 55.28%

- Houston, Texas: 2.26% average rate, $70,000 → $109,495.21, cumulative change of 56.42%

- Philadelphia, Pennsylvania: 2.26% average rate, $70,000 → $109,402.51, cumulative change of 56.29%

- St Louis, Missouri: 2.23% average rate, $70,000 → $106,460.58, cumulative change of 52.09%

- Chicago, Illinois: 2.17% average rate, $70,000 → $107,637.01, cumulative change of 53.77%

- Detroit, Michigan: 2.17% average rate, $70,000 → $107,578.92, cumulative change of 53.68%

San Diego, California experienced the highest rate of inflation during the 20 years between 2005 and 2025 (3.73%).

Detroit, Michigan experienced the lowest rate of inflation during the 20 years between 2005 and 2025 (2.17%).

Note that some locations showing 0% inflation may have not yet reported latest data.

Inflation by Country

Inflation can also vary widely by country. For comparison, in the UK £70,000.00 in 2005 would be equivalent to £133,573.70 in 2025, an absolute change of £63,573.70 and a cumulative change of 90.82%.

In Canada, CA$70,000.00 in 2005 would be equivalent to CA$105,875.20 in 2025, an absolute change of CA$35,875.20 and a cumulative change of 51.25%.

Compare these numbers to the US's overall absolute change of $44,623.30 and total percent change of 63.75%.

Inflation by Spending Category

CPI is the weighted combination of many categories of spending that are tracked by the government. Breaking down these categories helps explain the main drivers behind price changes.

Between 2005 and 2025:

- Gas prices increased from $1.82 per gallon to $3.23

- Bread prices increased from $1.00 per loaf to $1.88

- Egg prices increased from $1.21 per carton to $6.23

- Chicken prices increased from $1.03 per per 1 lb of whole chicken to $2.06

- Electricity prices increased from $0.09 per KwH to $0.18

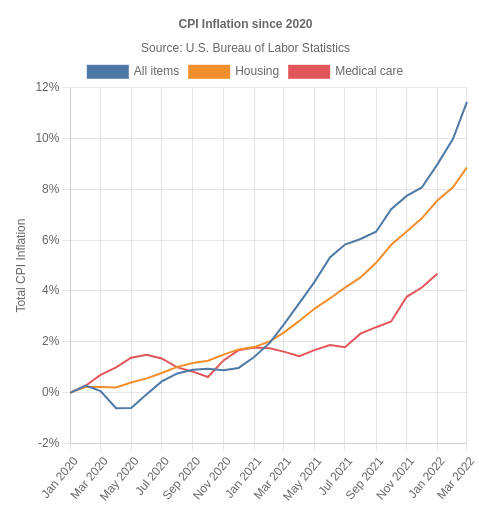

This chart shows the average rate of inflation for select CPI categories between 2005 and 2025.

Compare these values to the overall average of 2.50% per year:

| Category | Avg Inflation (%) | Total Inflation (%) | $70,000 in 2005 → 2025 |

|---|---|---|---|

| Food and beverages | 2.82 | 74.56 | 122,191.87 |

| Housing | 2.83 | 74.87 | 122,409.26 |

| Apparel | 0.49 | 10.24 | 77,164.56 |

| Transportation | 2.23 | 55.54 | 108,877.59 |

| Medical care | 2.91 | 77.38 | 124,163.02 |

| Recreation | 1.26 | 28.51 | 89,955.96 |

| Education and communication | 1.27 | 28.76 | 90,134.27 |

| Other goods and services | 3.03 | 81.71 | 127,197.61 |

The graph below compares inflation in categories of goods over time. Click on a category such as "Food" to toggle it on or off:

For all these visualizations, it's important to note that not all categories may have been tracked since 2005. This table and charts use the earliest available data for each category.

How to calculate inflation rate for $70,000 since 2005

Our calculations use the following inflation rate formula to calculate the change in value between 2005 and today:

CPI today CPI in 2005

×

2005 USD value

=

Today's value

Then plug in historical CPI values. The U.S. CPI was 195.3 in the year 2005 and 319.799 in 2025:

319.799195.3

×

$70,000

=

$114,623.30

$70,000 in 2005 has the same "purchasing power" or "buying power" as $114,623.30 in 2025.

To get the total inflation rate for the 20 years between 2005 and 2025, we use the following formula:

CPI in 2025 - CPI in 2005CPI in 2005

×

100

=

Cumulative inflation rate (20 years)

Plugging in the values to this equation, we get:

319.799 - 195.3195.3

×

100

=

64%

Alternate Measurements of Inflation

There are multiple ways to measure inflation. Published rates of inflation will vary depending on methodology. The Consumer Price Index, used above, is the most common standard used globally.

Alternative measurements are sometimes used based on context and economic/political circumstances. Below are a few examples of alternative measurements.

Personal Consumption Expenditures (PCE) Inflation

The PCE Price Index is the U.S. Federal Reserve's preferred measure of inflation, compiled by the Bureau of Economic Analysis. It measures the change in prices of goods and services purchased by consumers.

The PCE Price Index changed by 2.14% per year on average between 2005 and 2025. The total PCE inflation between these dates was 52.68%. In 2005, PCE inflation was 2.88%.

This means that the PCE Index equates $70,000 in 2005 with $106,878.12 in 2025, a difference of $36,878.12. Compare this to the standard CPI measurement, which equates $70,000 with $114,623.30. The PCE measured -11.06% inflation compared to standard CPI.

For more information on the difference between PCE and CPI, see this analysis provided by the Bureau of Labor Statistics.

Core Inflation

Also of note is the Core CPI, which uses the standard CPI but omits the more volatile categories of food and energy.

Core inflation averaged 2.43% per year between 2005 and 2025 (vs all-CPI inflation of 2.50%), for an inflation total of 61.78%. In 2005, core inflation was 2.17%.

When using the core inflation measurement, $70,000 in 2005 is equivalent in buying power to $113,247.89 in 2025, a difference of $43,247.89. Recall that the converted amount is $114,623.30 when all items including food and energy are measured.

Chained Inflation

Chained CPI is an alternative measurement that takes into account how consumers adjust spending for similar items. Chained inflation averaged 2.24% per year between 2005 and 2025, a total inflation amount of 55.71%.

According to the Chained CPI measurement, $70,000 in 2005 is equal in buying power to $109,000.31 in 2025, a difference of $39,000.31 (versus a converted amount of $114,623.30/change of $44,623.30 for All Items).

In 2005, chained inflation was 2.92%.

Comparison to S&P 500 Index

The average inflation rate of 2.50% has a compounding effect between 2005 and 2025. As noted above, this yearly inflation rate compounds to produce an overall price difference of 63.75% over 20 years.

To help put this inflation into perspective, if we had invested $70,000 in the S&P 500 index in 2005, our investment would be nominally worth approximately $466,716.63 in 2025. This is a return on investment of 566.74%, with an absolute return of $396,716.63 on top of the original $70,000.

These numbers are not inflation adjusted, so they are considered nominal. In order to evaluate the real return on our investment, we must calculate the return with inflation taken into account.

The compounding effect of inflation would account for 38.93% of returns ($181,694.61) during this period. This means the inflation-adjusted real return of our $70,000 investment is $215,022.02. You may also want to account for capital gains tax, which would take your real return down to around $182,769 for most people.

| Original Amount | Final Amount | Change | |

|---|---|---|---|

| Nominal | $70,000 | $466,716.63 | 566.74% |

| Real Inflation Adjusted | $70,000 | $285,022.02 | 307.17% |

Information displayed above may differ slightly from other S&P 500 calculators. Minor discrepancies can occur because we use the latest CPI data for inflation, annualized inflation numbers for previous years, and we compute S&P price and dividends from January of 2005 to latest available data for 2025 using average monthly close price.

For more details on the S&P 500 between 2005 and 2025, see the stock market returns calculator.

Data source & citation

Raw data for these calculations comes from the Bureau of Labor Statistics' Consumer Price Index (CPI), established in 1913. Price index data from 1774 to 1912 is sourced from a historical study conducted by political science professor Robert Sahr at Oregon State University and from the American Antiquarian Society. Price index data from 1634 to 1773 is from the American Antiquarian Society, using British pound equivalents.

You may use the following MLA citation for this page: “$70,000 in 2005 → 2025 | Inflation Calculator.” Official Inflation Data, Alioth Finance, 5 May. 2025, https://www.officialdata.org/us/inflation/2005?amount=70000.

Special thanks to QuickChart for their chart image API, which is used for chart downloads.

in2013dollars.com is a reference website maintained by the Official Data Foundation.

| Cumulative price change | 63.75% |

| Average inflation rate | 2.50% |

| Converted amount $70,000 base | $114,623.30 |

| Price difference $70,000 base | $44,623.30 |

| CPI in 2005 | 195.300 |

| CPI in 2025 | 319.799 |

| Inflation in 2005 | 3.39% |

| Inflation in 2025 | 2.39% |

| $70,000 in 2005 | $114,623.30 in 2025 |